Understanding Appraisal Waivers

For homebuyers and real estate professionals, the concept of an Appraisal Waiver, also known as Value Acceptance, is becoming increasingly relevant in today’s mortgage process. These waivers are issued through Automated Underwriting Systems (AUS), specifically Desktop Underwriter (DU) for Fannie Mae and Loan Product Advisor (LPA) for Freddie Mac.

What is an Appraisal Waiver?

A appraisal waiver allows a borrower to bypass the traditional home appraisal requirement, expediting the loan approval process while potentially saving hundreds of dollars in appraisal fees. Instead of requiring an appraisal, the lender relies on a database of recent appraisals and market data stored within Fannie Mae’s Collateral Underwriter and Freddie Mac’s property valuation models to confirm the property’s value.

How Value Acceptance is Determined

When a lender submits a loan application through DU or LPA, the system evaluates the borrower’s financial profile and the property’s eligibility for a waiver. If the system deems the value of the home to be sufficiently supported by existing data, it will return an eligibility determination for Value Acceptance.

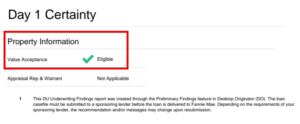

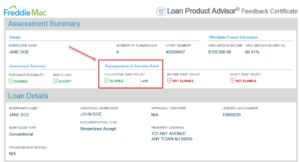

Here are examples of how value acceptance is displayed in the automated underwriting findings:

- Fannie Mae’s Desktop Underwriter (DU) shows a “Value Acceptance – Eligible” message in the Property Information section.

- Freddie Mac’s Loan Product Advisor (LPA) provides a similar determination under Representation & Warranty Relief for Collateral, marked as “Eligible” with “ACE” (Automated Collateral Evaluation).

Why This Matters for Real Estate Agents

Real estate agents who receive copies of pre-approval letters with AUS findings attached may notice these terms. Understanding what they mean can help set proper expectations for buyers and sellers.

One key term to understand is Representation & Warranty Relief. This means that when value acceptance is granted, the lender does not need to represent, warrant (guarantee), or prove the value of the property. This is because Fannie Mae or Freddie Mac already has sufficient data from recent appraisals in their databases to support the valuation. This significantly reduces risk for lenders and allows for a faster, more streamlined mortgage process.

The Importance of Running Both DU and LPA

It is a best practice for lenders and loan officers to run both DU and LPA findings for every loan file. This is because it is entirely possible for one system to grant value acceptance while the other does not.

For real estate agents, this highlights an important factor when referring buyers to lenders—not all lenders work with both Fannie Mae and Freddie Mac. If a lender only originates loans through one agency and does not check both systems, a borrower could miss out on a potential appraisal waiver that could save time and money.

Conclusion

Appraisal Waivers are a valuable tool in today’s mortgage lending environment, offering cost and time savings for borrowers while reducing risk for lenders. Real estate professionals should familiarize themselves with these terms and the implications of Representation & Warranty Relief, as well as encourage buyers to work with lenders who have access to both DU and LPA to maximize their chances of securing value acceptance and an appraisal waiver.

By understanding how these automated systems work, agents and buyers alike can navigate the mortgage process with greater confidence and efficiency.