Understanding Fannie Mae Loan Level Price Adjustments (LLPAs)

When it comes to conventional mortgages, many borrowers are unaware of an important cost factor known as Loan Level Price Adjustments (LLPAs). Whether you’re a first-time homebuyer or a seasoned real estate investor, it’s crucial to understand how these fees impact your mortgage rates and overall borrowing costs.

Both Fannie Mae and Freddie Mac, the government-sponsored entities that back a large portion of U.S. mortgages, charge LLPAs on all conventional loans. These risk-based fees are passed on to lenders and, ultimately, to you as the consumer. Let’s break down how LLPAs work and why they matter to your mortgage.

What Are Loan Level Price Adjustments?

LLPAs are essentially extra fees or adjustments added to the cost of your loan based on certain risk factors. These factors include:

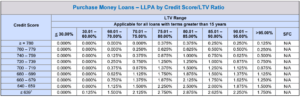

- Credit score (FICO score)

- Loan-to-value ratio (LTV), or the percentage of the loan compared to the value of the home

- Type of loan (e.g., investment property vs. primary residence)

- Other risk factors, such as the type of property or the loan term

The general rule of thumb is: the riskier the loan, the higher the cost. For example, if you have a lower credit score or are putting down a smaller down payment, you can expect higher LLPAs. Conversely, if you have a higher credit score and a larger down payment, the LLPAs will be lower.

How LLPAs Affect Your Mortgage

These fees are charged as a percentage of the loan amount and are applied cumulatively. That means the LLPAs from multiple risk factors can add up, making your loan more expensive. The key thing to note here is that LLPAs are the same across all lenders who sell conventional loans to Fannie Mae or Freddie Mac. Whether you go to Bank A or Bank B, the LLPAs applied by Fannie Mae are consistent across the board.

Here’s an important takeaway: even though LLPAs affect your overall mortgage cost, they won’t vary based on the lender you choose for a conventional loan. These are set fees passed on from Fannie Mae or Freddie Mac, not subject to negotiation between lenders.

The Impact of FICO Scores and LTV Ratios

One of the main factors driving LLPAs is your FICO score. The lower your score, the higher your perceived risk to the lender, and therefore, the higher your LLPA fees. Conversely, a high credit score will reduce the fees.

Similarly, Loan-to-Value (LTV) ratios also play a significant role. Loans with higher LTV ratios—meaning you’re borrowing more money relative to the home’s value—are riskier for the lender. As a result, LLPAs will increase as your LTV goes up.

However, there’s an interesting twist when LTV exceeds 80%. At this point, private mortgage insurance (PMI) becomes a requirement, reducing the lender’s risk. For example, loans with a 97% LTV (where the borrower puts down just 3%) may actually see lower LLPA costs because PMI offsets some of the risk. It’s worth noting that while PMI can reduce the costs from Fannie Mae, the PMI itself is an added cost, and it is also sensitive to your credit score.

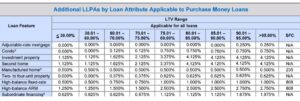

Additional Risk-Based LLPAs

LLPAs don’t just apply to FICO scores and LTV ratios. There are other risk factors that can trigger LLPAs, regardless of your credit score. These include:

- Whether you’re buying an investment property or a second home

- The type of property (e.g., condo vs. single-family home)

- The loan term (e.g., 15-year vs. 30-year mortgage)

In these cases, larger down payments can help reduce the costs. Just as with credit scores and LTV ratios, these adjustments are rooted in risk management. Fannie Mae and Freddie Mac want to mitigate the risk of default, so the more equity you have in your home upfront, the lower the risk and the lower the LLPAs.

Navigating LLPAs and Your Mortgage Strategy

Understanding LLPAs is essential for making informed decisions about your mortgage. By improving your credit score and increasing your down payment, you can significantly reduce the fees associated with these price adjustments. However, even with LLPAs, conventional loans remain a competitive option for many borrowers, especially when balanced with PMI and other potential costs.

It’s important to work closely with your lender to understand how LLPAs apply to your unique situation. This can help you get the most favorable terms and ensure you’re making the best financial decision for your future.