FHA Loans: Understanding the Impact of Mortgage Insurance on Interest Rates

When comparing different mortgage options, borrowers often weigh the pros and cons of FHA loans versus conventional loans. One of the biggest distinctions between the two is the way they handle pricing adjustments and mortgage insurance. While conventional loans often come with Loan Level Price Adjustments (LLPAs), as outlined in our post about Fannie Mae LLPAs, FHA loans take a different approach, which can lead to lower overall interest rates.

Let’s break down how FHA loans work and why they might be the best option for certain borrowers.

No LLPAs on FHA Loans

A key advantage of FHA loans is that they do not have LLPAs. LLPAs are risk-based fees charged on conventional loans based on factors like your credit score and loan-to-value (LTV) ratio. For borrowers with lower credit scores or smaller down payments, LLPAs can significantly increase the cost of a conventional mortgage, making an FHA loan a more appealing option.

Because FHA loans don’t have these risk-based adjustments, they often come with lower interest rates, making them an attractive option for buyers with less-than-perfect credit. However, FHA loans do come with mandatory mortgage insurance that you’ll need to account for.

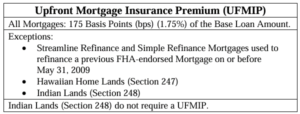

FHA Mortgage Insurance: UFMIP and Annual Premium

While FHA loans don’t have LLPAs, they do require two types of mortgage insurance:

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time fee equal to 1.75% of the loan amount, and it is automatically financed into your mortgage. Unlike other fees, this premium cannot be paid in cash at closing—it’s added to your loan balance, effectively increasing the amount you borrow.

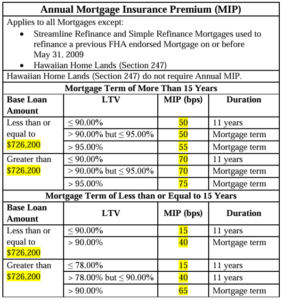

- Annual Mortgage Insurance Premium (MIP): This is recalculated every year as a percentage of the loan amount and is paid monthly. The percentage depends on your LTV ratio and loan amount, but for most FHA loans with a minimum down payment of 3.5%, the annual premium is 0.55%.

While FHA interest rates may be lower than conventional rates, the annual premium functions similarly to an additional cost to your mortgage. For example, if your base interest rate is 5.750% and your annual premium is 0.55%, the effective rate on your loan is 6.30%.

The Lifetime of FHA Mortgage Insurance

One key detail about FHA loans is the length of time you’re required to pay the annual mortgage insurance premium:

- If your loan’s LTV is greater than 90% (meaning you put down less than 10%), the mortgage insurance remains for the life of the loan.

- For loans with an LTV of 90% or less (with a down payment of at least 10%), the annual mortgage insurance cancels after 11 years (132 months).

This is important to consider, as it means FHA mortgage insurance could remain a cost for as long as you hold the loan, unlike conventional loans, where private mortgage insurance (PMI) can be removed once you reach 20% equity in the home.

Comparing FHA Loans to Conventional Loans

One of the most important comparisons borrowers make is between FHA loans and conventional loans. For borrowers with lower credit scores, FHA loans tend to offer a lower effective interest rate, even when conventional loans do not require PMI. This is because conventional loans come with LLPAs that can significantly raise interest rates for those with less-than-perfect credit.

Take, for instance, an FHA loan with a base rate of 5.750% and an annual premium of 0.55%. The effective rate on this loan would be 6.30%. Even though you are paying mortgage insurance, the total cost of the FHA loan could still be lower than a conventional loan with a higher interest rate due to LLPAs.

Considering the FHA Upfront Premium

When evaluating FHA loans, it’s important to factor in the Upfront Mortgage Insurance Premium (UFMIP) of 1.75%. While this premium is financed into the loan, it increases the loan amount and the amount of interest you’ll pay over time.

For example, on a $200,000 loan, the UFMIP adds $3,500 to the loan balance, making your total loan amount $203,500. While this results in a larger loan amount, if the effective rate and total payment on the FHA loan are still lower than a conventional loan, the FHA option may result in lower monthly payments and less interest paid over the life of the loan.

Bottom Line: Focus on Total Payment

At the end of the day, your monthly mortgage payment is what truly matters. Whether you’re choosing an FHA loan with mortgage insurance or a conventional loan with LLPAs, the goal is to secure a financing option that offers the lowest total payment.

It’s important to compare not only interest rates but also effective rates, mortgage insurance costs, and total loan amounts when evaluating your mortgage options. The FHA loan, despite its upfront and ongoing insurance premiums, may end up being the more cost-effective option for many borrowers—particularly those with lower credit scores.

For more information on how conventional loans are priced and the role of Loan Level Price Adjustments, be sure to check out our blog post on Fannie Mae LLPAs. Understanding both FHA and conventional loan options will help you make the best decision for your financial future.