Temporary buydowns provide temporary relief from higher interest rates by allowing the buyer to temporarily make a lower payment based upon a reduced interest rate during the first few years of a mortgage. The buyer is always underwritten and approved with the full interest rate, but the hope is that rates come down and allow for a refinance in the future.

There are several buydown options with the most common being a 1-0 Buydown or 2-1 Buydown. In a 1-0 buydown, the first-year payment is calculated using a rate 1.00% lower than the interest rate and then reverts to the full rate and payment in year 2. In a 2-1 buydown, the first-year payment is calculated using a rate 2.00% lower than the interest rate in the first year, 1.00% lower in the 2nd year, and then reverts to the full rate and payment in year 3. There are other ways to structure a temporary buydown as well:

- 1-0 Buydown: Buydown of 1% in year one, then back to the original locked rate in year 2 for the remaining term.

- 1-1 Buydown: Buydown of 1% in year one and year two, then back to the original locked rate in year 3 for the remaining term.

- 2-1 Buydown: Buydown of 2% in year one, 1% in year two, then back to the original locked rate in year 3 for the remaining term.

- 1.5-0.5 Buydown: Buydown of 1.5% in year one, 0.5% in year two, then back to the original locked rate in year 3 for the remaining term.

- 3-2-1 Buydown: Buydown of 3% in year one, 2% in year two, 1% in year three, then back to the original locked rate in year 4 for the remaining term.

In all these instances, only the payment is being temporarily reduced, not the interest rate. To make this work, the seller issues a credit at closing to fund an escrow account, and the funds are used to pay the difference between the temporary payment and the full payment during each month of the temporary buydown period. If the loan is paid off or refinanced before the end of the temporary buydown period, the remaining funds are applied as a principal reduction on the loan balance.

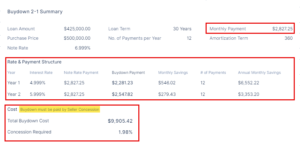

Here is an example of what a 2-1 temporary buydown would look like on a $425,000 loan amount with an interest rate of 6.999%:

In year one, the P&I payment is based upon 4.999%, temporarily reducing it to $2,281.23 and saving $546.02 per month, or $6,552.22 over the first year.

In year two, the P&I payment is based upon 5.999%, temporarily reducing it to $2,547.82 and saving $279.43 per month, or $3,353.20 over the second year.

In year three and for the remainder of the loan term, the payment is based upon 6.999% with a payment of $2,827.25

The total savings over the first 2 years is $6,552.22 + $3,353.20 = $9,905.42; this is the amount of the required seller credit (1.98% of the purchase price).

Author: Chris DeMatteis, NMLS ID 214872